On 29 May 2025, the largest borrower on Debitum bought a piece of Latvian forest for EUR 16,500 from its former parent company. The parent company had bought it from a local landowner 105 days earlier. For EUR 537. This was one of 254 such properties.

The pitch is simple. A MiFID II-regulated investment platform. Nine active loan originators, most of them buying and trading Latvian forestland. Investors earn 10-15% backed by real, appreciating assets. Oversight and diversification built in.

Three things are wrong with this story.

First, investors were told there’s a profitable buyer out there paying above market for forestland that’ll pay for all of this. There is. It’s them. Retail investors are the ones buying forests at inflated prices from companies belonging to the same network tied to the platform. Of every euro spent this way buying forestland, roughly 34 cents is markup for the insiders.

Second, the platform is not a marketplace of independent issuers. Seven of nine are connected to the same network of companies. And they constantly buy assets from other companies owned by the same people.

Third, the regulation covers the platform. It does not cover what happens underneath it. The issuers and intermediaries operate through a web of undisclosed related-party transactions, false registry declarations, and prospectus omissions that the regulator either missed or chose not to act on.

Executive Summary

Debitum isn’t really a marketplace at all. The only two independent issuers on the platform are Triple Dragon and Evergreen Capital. Every single other one traces back to the same extended family network of owners, executives, and related companies tied to Debitum. That network accounts for 87% of Debitum’s EUR 58.4M outstanding portfolio.

The largest issuer is the Latvian Forest Development Fund (LFDF), with EUR 37.9M in outstanding obligations to retail investors. That’s 65% of the entire platform in a single entity.

At the center is Guntars Galvanovskis, a former member of the Latvian parliament. He owns the three largest intermediaries that sell land to LFDF at marked-up prices. His wife owns the fourth. A man who married into the family runs a fifth. The platform owner used to sit on their boards. LFDF’s beneficial owner is the sitting Parliamentary Secretary at the Ministry of Finance. Seven people sit on both sides of the table.

What LFDF and other network issuers do with investor money is something to behold:

- 81% internal trading. LFDF bought 81% of its properties from companies belonging to the same owner network. That network around Galvanovskis bought the properties, held them for an average of 203 days, then sold them to LFDF at a 50% markup.

- EUR 24M gap. LFDF reports EUR 36.8M in inventory on its 2025 operating balance. Land registry records show transaction values for 652 of its 680 properties, totaling EUR 12.2M. The remaining EUR 24.6M has no corresponding entry in public land records.

- Two-tier pricing: 251% vs 7%. One land trading intermediary acquired properties both for LFDF and the family founder’s personal company. Markup for LFDF? 251%. Markup for the founder? 7%.

- Timber extraction. Another family-owned company bought 25 forested properties and resold them at a mere 2% markup to LFDF. Yet that same company reported EUR 316,630 in logging revenue that year, raising the obvious question of whether the underlying value of the land was extracted before retail investors bought it.

- Fourteen false filings. Every entity in the family filed at least one annual report or prospectus that omitted or denied related-party relationships contradicted by other public records.

- Politically Exposed Person (PEP) non-disclosure. LFDF’s beneficial owner, Jānis Upenieks, is the sitting Parliamentary Secretary at the Ministry of Finance and has held PEP-qualifying positions since 2011. Under EU anti-money laundering rules (Directive 2015/849, Article 20), the platform is required to identify him as a Politically Exposed Person and apply enhanced due diligence. The prospectus has a section on “Beneficial Owner Interest Risk.” It does not mention that the beneficial owner holds a senior government position.

- Collateral exclusion. LFDF’s and Baltic Terra Capital’s prospectuses explicitly exclude the land portfolio from investor collateral. The primary asset of a forestry fund is not pledged.

Some movies start with “based on a true story.” This is more than based on a true story. It’s based on government registries, regulator-approved prospectuses, the companies’ own filings, and the occasional real estate listing that nobody seems to want to buy. 652 properties with individual transaction records, 52 annual reports across 12 companies, some going back seven years. Registry and public data on 23 individuals: family members, a finance ministry official, platform executives, a shared accountant, and other associates whose names kept surfacing in the same company filings.

Every document cited in this report is publicly sourced. The analytical conclusions drawn from those records are mine.

Who is Debitum

Debitum operates through SIA DN Operator (reg. 42103092209), a MiFID II-licensed investment brokerage owned by Ingus Salmiņš via SIA ZIdea. It lists nine active loan originators. Seven are connected through ownership, governance, or employment to the same network of companies centered on Guntars Galvanovskis. The other two aren’t.

Sources:

- https://company.lursoft.lv/en/dn-operator/42103092209

- https://company.lursoft.lv/en/zidea/40203138540

The loan originators

Here are the nine loan originators and what they do:

- LFDF (Latvian Forest Development Fund): buys forestland with investor money. 65% of the platform. Owned by Jānis Upenieks. (Source: https://company.lursoft.lv/en/latvijas-meza-attistibas-fonds/40203475516)

- Sandbox Funding: loan originator that bundles loans into asset-backed securities. Investors don’t usually see which borrower gets their money. Co-owned by Salmiņš. (Source: https://company.lursoft.lv/en/sandbox-funding/40203473712)

- AS JUNO (listed as JSC Juno on the platform): land trader. Sells forest to LFDF at 79% markup. 100% Galvanovskis. (Source: https://company.lursoft.lv/en/juno/40203024821)

- Baltic Terra Capital: land fund and Debitum note issuer. Buys forested land, resells it to LFDF at 2% land markup while reporting EUR 316,630 in timber revenue. Owned by Jānis Lezdiņš. (Source: https://company.lursoft.lv/en/baltic-terra-capital/40203653737)

- Juno Finance: upstream lender. Finances LK CARE (251% markup seller to LFDF). JUNO subsidiary. (Source: https://company.lursoft.lv/en/juno-finance/50203459621)

- Bono House: built one house, never sold it. 100% subsidiary of BONO. (Source: https://company.lursoft.lv/en/bono-house/40203370560)

- Foresto: land trader. Sells to LFDF. Owned by Andžejevskis (married into the Galvanovskis family). (Source: https://company.lursoft.lv/en/foresto/40203311266)

- Evergreen Capital (Estonia): appears genuinely independent. (Source: https://debitum.investments/en/partners/evergreen-capital)

- Triple Dragon (UK): appears genuinely independent. (Source: https://debitum.investments/en/partners/triple-dragon)

The people

The broader network spans 23 individuals. Only three of them work at the platform itself.

Ingus Salmiņš, platform owner. Sat on the boards of BONO and AS JUNO before acquiring Debitum in 2023. Co-founded Foresto. Borrows from Sandbox at 1.66% while investors fund it at 10-15%. (Source: https://www.lursoft.lv/meklet?q=Salmiņš+Ingus&l=en, paywalled)

Ēriks Reņģītis, former co-owner (~33%, exited October 2025). Simultaneously served as CFO of BONO Group. During Debitum’s fastest growth, one person sat on both sides. (Source: https://www.lursoft.lv/meklet?q=Reņģītis+Ēriks&l=en, paywalled)

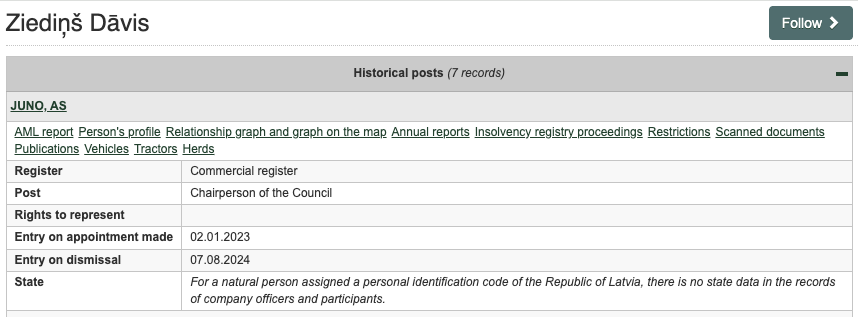

Dāvis Ziediņš, Head of Business Development. Describes joining Debitum as “a 1-month advisory gig.” Lursoft shows he sat on the AS JUNO supervisory council for five years. From January 2023 to August 2024 he even chaired it:

That position is not on his LinkedIn.

Sources:

- https://www.linkedin.com/in/davisziedins/

- https://www.lursoft.lv/meklet?q=Ziediņš+Dāvis&l=en (paywalled)

The address

Debitum Investments is registered at Dzirnavu iela 67, Rīga. (Source: https://company.lursoft.lv/en/dn-operator/42103092209)

So is Sandbox Funding, the second-largest loan originator. (Source: https://company.lursoft.lv/en/sandbox-funding/40203473712)

Both moved there from Ūnijas iela 8 k-7, Rīga. That’s the office of AS JUNO, the largest LFDF intermediary, which charged a total markup of EUR 2,508,929 on the land it sold to LFDF. (Source: https://company.lursoft.lv/en/juno/40203024821)

What happens on Debitum?

The platform presents itself as a marketplace of independent issuers buying real assets. The land registry disagrees.

81% internal trading

LFDF bought 528 of its 652 price-tracked properties from five companies controlled by the Galvanovskis family. Where both sides of the price chain are visible (484 of those 528), 34 cents of every euro LFDF paid went to the family as markup. The land registry proves it: Latvia’s public records include transaction prices for both buyer and seller on the same parcel. I obtained the records for every property in LFDF’s portfolio. (Source: https://www.lursoft.lv/en/vzd/jp-real-estates/index/40203475516)

| Intermediary | Properties with price history | LFDF Paid | Prior Cost | Markup |

|---|---|---|---|---|

| AS JUNO | 239 | EUR 5,237,497 | EUR 2,917,895 | 79% |

| SIA BONO | 150 | EUR 3,326,567 | EUR 2,530,774 | 31% |

| SIA Dizozols | 40 | EUR 1,067,397 | EUR 462,864 | 131% |

| SIA Foresto | 30 | EUR 296,843 | EUR 594,445 | -50% |

| SIA Baltic Terra Capital | 25 | EUR 319,580 | EUR 312,858 | 2% |

| Family total | 484 | EUR 10,247,884 | EUR 6,818,836 | 50% |

Of the 528 network properties, 484 have both LFDF’s purchase price and the seller’s acquisition cost in the land registry. For the remaining 44, the registry shows LFDF’s price but not what the family company paid. All figures in the table use only those 484 matched-pair properties.

The family intermediaries held these properties for an average of 203 days and charged a 50% markup. For comparison, non-network sellers held for an average of 4.6 years and charged a 28% markup. To put that in annual terms: non-network sellers saw an annualized return of 5.6%. Network intermediaries saw 96.9%.

Here is who these companies are:

AS JUNO (100% Galvanovskis): 254 properties, 79% markup. LFDF’s own former parent company. JUNO alone collected over EUR 2.3 million in verified markups from a retail-investor-funded entity that used to be its subsidiary. (Source: https://company.lursoft.lv/en/juno/40203024821)

SIA BONO (80% Kate Glika, Galvanovskis’s wife): 167 properties, 31% markup. EUR 56.8M revenue, EUR 2.75M profit, EUR 16.1M equity, 51 employees. Zero exposure to Debitum investors. Its subsidiary Bono House, the one that does face investors, has negative equity of EUR 767,389. The profitable parent has no exposure to Debitum investors. (Source: https://company.lursoft.lv/en/bono/44103079618)

SIA Dizozols (100% Galvanovskis): 45 properties, 131% markup. (Source: https://company.lursoft.lv/en/dizozols/40203227482)

SIA Foresto (100% Juris Andžejevskis, married into the Galvanovskis family): 37 properties, -50% markup. The only exception here. Andžejevskis chairs the board of BONO. (Source: https://company.lursoft.lv/en/foresto/40203311266)

SIA Baltic Terra Capital (100% Jānis Lezdiņš, AS JUNO’s Head of Sales): 25 properties, 2% land markup. Also a Debitum note issuer. (Source: https://company.lursoft.lv/en/baltic-terra-capital/40203653737)

Baltic Terra Capital’s 2% land markup is not what it appears. It acquired all 25 properties on 29-30 July 2025 and resold them to LFDF 42 days later, accounting for 74% of Baltic Terra Capital’s total land sales. Baltic Terra Capital’s own annual report also reports EUR 316,630 in timber revenue. Which properties the timber came from isn’t in the public record, but the structure fits a straightforward sequence: buy forested land, log it, and sell the land afterwards to LFDF. (Source: https://company.lursoft.lv/en/baltic-terra-capital/40203653737)

The markup on those transactions, over EUR 4 million verified across JUNO, BONO, and Dizozols, flows to companies that have no obligation to Debitum investors. No notes, no pledges, no buyback commitments. Once LFDF pays the marked-up price, the money is gone.

A case study: contract PL-29-05/2025/3

Land registers list contract numbers, allowing us to determine which properties were sold together. Let’s have a look at this specific contract to see what happened.

On 29 May 2025, LFDF purchased seven properties from AS JUNO under a single contract:

| Cadastre | Name | JUNO Paid | LFDF Paid | Markup | Days Held |

|---|---|---|---|---|---|

| 44720030034 | (unnamed) | EUR 537 | EUR 16,500 | 2,973% | 105 |

| 44700030270 | (unnamed) | EUR 350 | EUR 7,000 | 1,900% | 139 |

| 88700020041 | Jaunčakšu mežs | EUR 893 | EUR 14,000 | 1,468% | 127 |

| 62720040007 | Strēļi | EUR 1,116 | EUR 14,500 | 1,199% | 105 |

| 68860020099 | Laši | EUR 1,422 | EUR 17,000 | 1,096% | 150 |

| 68600010432 | Vecie Runči | EUR 4,388 | EUR 52,000 | 1,085% | 100 |

| 66880100012 | Vecupītes | EUR 1,750 | EUR 9,000 | 414% | 65 |

| 7 properties | EUR 10,456 | EUR 130,000 | 1,143% |

This is one contract. Seven properties. Sold for 12x after an average holding period of 113 days. (Source: https://www.lursoft.lv/en/vzd/jp-real-estates/index/40203475516)

Case study: 251% for investors, 7% for the founder

A small intermediary called LK CARE reveals the pricing gap. It sold land to both sides: to LFDF, the investor-funded entity, and to Ozolu meži, Galvanovskis’s personal vehicle. Markup for LFDF? 251%. For Galvanovskis? 7%.

If Latvian forestland appreciates at 5.6% per year (the rate non-network sellers averaged), it would take 23 years to produce a 251% return. Thanks to LFDF’s generosity with other people’s money, LK CARE managed it in twelve days.

Sources:

- https://www.lursoft.lv/en/vzd/jp-real-estates/index/40203475516

- https://company.lursoft.lv/en/lk-care/41503081019

- https://company.lursoft.lv/en/ozolu-mezi/44103097153

Where did the missing EUR 24.6 million go?

LFDF’s unaudited operating balance at 31 December 2025 reports EUR 36,793,040 in inventory. The land registry records EUR 12,229,829 in purchase prices for 652 of LFDF’s 680 properties as of March 2026, including 24 acquired after the balance sheet date. The gap: EUR 24.6 million. Two-thirds of reported inventory has no trace in the land registry. At year-end 2024, book inventory was 2.2 times the recorded land cost. A year later, 3.0 times. Whatever is being added to inventory beyond land prices is growing faster than the land purchases themselves. (Source: https://company.lursoft.lv/en/latvijas-meza-attistibas-fonds/40203475516)

Some of that gap is expected. There are 28 properties for which there is no recorded purchase price; it’s fair to assume those weren’t free. In addition, under Latvian Generally Accepted Accounting Principles (GAAP), inventory at cost can include timber purchase agreements, forestry management fees, and service commissions, none of which appear in the land registry. LFDF is a forestry fund. Timber rights may represent a significant share of the asset value.

That’s the optimistic reading. The less optimistic reading notes that the same network already collecting a 50% markup on land sales would also be in a position to collect commissions for “brokering” deals between two companies that sit in the same office, or management fees for services rendered by entities sharing the same owner. Does that happen? We don’t know. What we do know is that nothing currently visible to outsiders breaks down where the EUR 24.6 million went.

LFDF has four employees. It outsources all forestry operations to unnamed “trusted service providers.” In 2025, LFDF reported EUR 10.8 million in revenue and EUR 2.9 million in other operating expenses. The prospectus does not name the service providers. Given that 81% of the land comes from five family companies, the odds that the “trusted service providers” are also family entities are … high. (Source: https://www.lfdf.eu/documents)

On paper, LFDF made EUR 1.6 million in profit in 2025. That number assumes the EUR 36.8 million portfolio is worth what LFDF paid for it. If the verified related-party markups (EUR 4.3 million across 484 properties) reflect value extraction rather than genuine value creation, LFDF’s reported profit turns into a EUR 2.7 million loss. We don’t have independent valuations to settle that question. What we do know: the intermediaries held the land for an average of 203 days, added no publicly visible improvements, and charged an additional 50% when they sold it. If the remaining EUR 24.6 million isn’t all backed by real asset value, the rate at which funds leave the company gets scary very quickly. (Source: https://debitum.investments/blog/lfdf-and-debitum-in-2025-year-in-review/)

What the prospectus doesn’t say

The regulator-approved LFDF prospectus discloses one of six related intermediaries: AS JUNO. It describes EUR 14.7 million in purchases from JUNO as “according to market conditions.” Land registry records show JUNO paid 56 cents for every euro LFDF spent. The prospectus does not disclose what JUNO paid. (Source: https://www.lfdf.eu/documents)

The other five intermediaries (BONO, Dizozols, Foresto, Baltic Terra Capital, LK CARE) are not mentioned at all. A less-scrutinized Juno Finance offering document voluntarily discloses that BONO is related to the family and that Reņģītis is its CFO. Both regulator-approved LFDF prospectuses omit BONO entirely. LK CARE, the 251% markup intermediary, is financed by Juno Finance, which raises capital on Debitum to “finance SMEs.” The SME it financed bought forest and sold it to LFDF at a 251% markup in twelve days. (Source: https://www.lursoft.lv/pledge/100209026)

289 properties. EUR 5.9 million. All connected to the same family. All absent from the prospectus Latvijas Banka approved.

The collateral that doesn’t cover the assets

Both the LFDF and Baltic Terra Capital prospectuses state: “The Collateral does not include mortgage over the Land Portfolio.” (Source: https://www.lfdf.eu/documents)

The primary asset of a forestry fund is land. The one thing that investors have no claim over: that same land. Because investors hold no mortgage over it, nothing prevents LFDF from pledging the land to someone else, including the family companies it already owes EUR 5.16 million to.

Who controls all of this?

Seven people control the platform, the issuers, the intermediaries, and the books. All roles below confirmed via the Latvian Commercial Register (Lursoft).

- Guntars Galvanovskis, former MP. Owns AS JUNO (79% markup on LFDF), Dizozols (131%), and 85% of Ozolu meži. The center of the network.

- Kate Glika, his wife. Owns 80% of BONO, the second-largest intermediary (31% markup). Juno Finance’s own Terms of Issue names her as “a related party of the Issuer’s beneficial owner Guntars Galvanovskis.”

- Juris Andžejevskis, married into the Galvanovskis family (wife’s maiden name: Galvanovska). Chairs BONO, owns Foresto, runs Bono House.

- Zane Galvanovska. Four board seats across the family network. Replaced Melderis on three of them on a single date. Her surname is the standard Latvian feminine form of Galvanovskis.

- Jānis Upenieks, beneficial owner of LFDF. Current Parliamentary Secretary at the Ministry of Finance. Acquired LFDF from Galvanovskis’s AS JUNO two months before his government appointment.

- Gatis Melderis, board member of AS JUNO, LFDF, and Intelligent Innovations simultaneously. Signed the LFDF prospectus.

- Jānis Lezdiņš, Head of Sales at AS JUNO, owner of Baltic Terra Capital, chairs Dizozols. Sells JUNO’s land at 79% markup while running his own issuer on the same platform.

Every person listed above holds at least one position at a company registered at one of two addresses: Beātes iela 5 in Valmiera (BONO, Bono House, Foresto, Ozolu meži) or Dzirnavu iela 67 in Rīga (Debitum, Sandbox Funding, AS JUNO). Galvanovskis could call Galvanovska, put each other on speakerphone, and have the entire network on one call without anyone leaving the office.

The family involvement isn’t new. P2P Empire, the only independent review site to dig into the structure, identified the same concentration pattern, mapped the management overlaps, and withdrew its rating of Debitum entirely.

Sources:

- https://www.lursoft.lv/address/valmieras-novads-valmiera-beates-iela-5-lv-4201

- https://www.lursoft.lv/meklet?q=Galvanovskis+Guntars&l=en (paywalled)

- https://www.lursoft.lv/meklet?q=Galvanovska+Zane&l=en (paywalled)

- https://www.lursoft.lv/meklet?q=Upenieks+Jānis&l=en (paywalled)

- https://www.lursoft.lv/meklet?q=Melderis+Gatis&l=en (paywalled)

- https://www.lursoft.lv/meklet?q=Lezdiņš+Jānis&l=en (paywalled)

Sandbox Funding

Sandbox Funding is the issuer with the second-highest amount currently owed to investors: EUR 9.5 million outstanding, 2 employees. Co-owned by Salmiņš (66.86% via ZIdea) and Reņģītis (33.14% via Amplo). The same Salmiņš who owns the platform. Debitum’s own blog describes Sandbox as “our fully controlled ally company” and says the shared ownership is something they’re “not hiding.”

Sources:

- https://company.lursoft.lv/en/sandbox-funding/40203473712

- https://debitum.investments/blog/partner-stories-sandbox-funding-our-key-loan-originator/

Investors don’t buy securities from Sandbox directly. Sandbox originates loans, then transfers the receivables to special purpose vehicles (SPVs) owned by DN Operator. Those SPVs issue the securities. Here is what sits underneath.

The only protection is a buyback clause. If a borrower defaults, the SPV can trigger a buyback, forcing Sandbox to repurchase the bad loan. Investors can’t trigger the buyback themselves, only the SPV can. And the SPV is owned by the same person who owns Sandbox. Sandbox has EUR 560,028 in equity against EUR 9.5 million in outstanding obligations. Salmiņš would be the one deciding whether to enforce the buyback against himself, bankrupting Sandbox in the process. (Source: https://company.lursoft.lv/en/sandbox-funding/40203473712)

Meanwhile, the platform owner borrows at 1.66%. Sandbox’s audited 2024 annual report (Note 7) discloses five loans totaling EUR 290,000 to ZIdea, Salmiņš’s personal holding company, at 1.66% annual interest. Investors fund Sandbox at 10-15%. Sandbox lends to its owner at 1.66%. Every euro of that loan costs Sandbox more to fund than it earns back. The loss lands on the balance sheet of the company whose buyback obligation is the only thing protecting investors.

Sources:

- https://company.lursoft.lv/en/sandbox-funding/40203473712

- https://company.lursoft.lv/en/zidea/40203138540

The borrowers identified through the pledge registry are all family entities. The prospectus does not disclose which borrowers receive Sandbox’s loans or which loans back which securities. Investors see “2,322 funded business loans” and a “0% default rate.” The Debitum blog names Bono House as a Sandbox partner. Commercial pledge registry research identified two more: Juno Finance and Foresto. All three are family entities. Juno Finance is a subsidiary of AS JUNO (100% Galvanovskis). Bono House is a subsidiary of BONO (Galvanovskis’s wife). Foresto is 100% owned by Andžejevskis, BONO’s chairman.

Sources:

- https://debitum.investments

- https://www.lursoft.lv/pledge/100209110

- https://www.lursoft.lv/pledge/100209111

- https://www.lursoft.lv/pledge/100209112

When investors look up loans offered by Sandbox on Debitum, this is what they see about the companies borrowing the funds: “5 underlying loans” to unnamed “SMEs registered in the EU and EEA.” No borrower names. No indication that every identified borrower is a company belonging to the same family network that runs the platform. One investor’s “SME loan” can quietly become another investor’s repayment, and nobody outside the network can tell the difference. (Source: https://debitum.investments/en/invest/a94b31c2-7963-450f-b44c-349d53fae0e8)

Where did the money come from?

One of the known borrowers is Bono House. It built a single residential property. It was put up for sale in 2023, more than a year before the house was finished. Nearly three years later, it’s still not sold. (Source: https://www.jamesedition.com/real_estate/sunisi-latvia/innovative-private-house-by-the-river-12903780)

Total revenue in four years of existence: EUR 111,570. Airbnb? Rent? Who knows. Certainly not from selling the house. (Source: https://company.lursoft.lv/en/bono-house/40203370560)

Yet it repaid EUR 989,980 in principal to Debitum investors at 12.67% interest. With whose money? (Source: https://debitum.investments/en/stats)

If we look at historic balance sheets, we see two separate debt lines. “Borrowings against bonds”: that’s what’s owed to Debitum investors, and “other borrowings” from an unnamed lender, which grew to EUR 1,501,471.

The balance sheet shows where the repayment money came from: borrowed from someone else. The annual reports don’t name the lender. No related-party transactions are reported. (Source: https://company.lursoft.lv/en/bono-house/40203370560)

So who would lend 1.5M to a company with nothing but an unsellable house worth a fraction of that?

The pledge registry might be a hint.

There is a company that holds a 7.5M pledge over Bono House: Sandbox. The family’s own originator. The originator that bundles up largely undisclosed loans and sells them to investors as “SME financing.” (Source: https://www.lursoft.lv/pledge/100209111)

The million dollar (okay, EUR 989,980) question is: did Sandbox, the platform’s “fully controlled ally,” use retail investor capital to bail out investors in a negative-equity, family-owned subsidiary that couldn’t sell its only asset... and called that an “SME loan”?

How is this possible?

MiFID II regulates the platform. It does not audit the filings of every company that issues securities through it. The system assumes those filings are accurate. They aren’t.

Fourteen false filings

Every entity in the family that I examined filed at least one annual report or prospectus that omitted, denied, or misrepresented related-party relationships that demonstrably existed at the time of filing. Latvian accounting law defines “related parties” by direct reference to IAS 24, which explicitly includes spouses and close family members. But even if it didn’t: five of these filings contradict themselves on the same page.

1. BONO’s annual reports, 2017 to 2024, all eight years: the related-party transaction field is blank. False. BONO’s own balance sheet carries EUR 2.8 million in related-company receivables, and it sold 167 properties to LFDF at a 31% markup. (Source: https://company.lursoft.lv/en/bono/44103079618)

2. AS JUNO’s annual reports, 2017 to 2024, all eight years: every related-party disclosure field left blank. False. The company’s own balance sheet reports EUR 5.3 million owed by related companies. Its own P&L reports EUR 240,000 in interest income from related companies. (Source: https://company.lursoft.lv/en/juno/40203024821)

3. Juno Finance’s 2023 annual report: “Sabiedrībai nav radniecīgo vai asociēto sabiedrību.” The company has no related or associated companies. False. The same report’s own P&L shows EUR 133 in interest income from related companies. Its own Terms of Issue describes the JUNO group structure. (Source: https://company.lursoft.lv/en/juno-finance/50203459621)

4. Ozolu meži’s 2024 annual report: “Sabiedrībai nav radniecīgo vai asociēto sabiedrību.” The company has no related or associated companies. False. 85% owned by Galvanovskis, who owns 100% of AS JUNO. Identical statutory language, identically false. (Source: https://company.lursoft.lv/en/ozolu-mezi/44103097153)

5. Dizozols’ annual reports, 2020 to 2024, all five years: related-party fields blank. False. The 2021 balance sheet shows EUR 621,000 payable to related companies. Dizozols sold 45 properties to LFDF at a 131% markup. (Source: https://company.lursoft.lv/en/dizozols/40203227482)

6. Intelligent Innovations’ annual reports, 2021 to 2024, all four years: every related-party field blank. False. The company holds a EUR 120 million pledge on LFDF shares. Its owner, Jānis Upenieks, is LFDF’s beneficial owner. (Source: https://company.lursoft.lv/en/intelligent-innovations/40203325336)

7. Foresto’s 2024 annual report: section 1.8.6, related-party obligations, deleted entirely. False. The 2023 report disclosed a related-company loan in that same section. Interest expense tripled. (Source: https://company.lursoft.lv/en/foresto/40203311266)

8. Baltic Terra Capital’s 2025 annual report: “No unrecorded rights or obligations.” False. Two EUR 120 million pledges were registered 12 days before the balance sheet date. 298 times total assets. (Source: https://company.lursoft.lv/en/baltic-terra-capital/40203653737)

9. Same report: “No significant events not reflected in the balance sheet.” False. Same two pledges. Same 12 days.

10. LFDF’s initial prospectus, January 2025: “No related-party transactions except JUNO financing.” False. The fund’s inventory consisted largely of land purchased from AS JUNO, its own former parent company, at a 79% markup. (Source: https://www.lfdf.eu/documents)

11. LFDF’s succeeding prospectus, August 2025: corrected the JUNO omission. Omitted everything else. Four intermediaries (BONO, Dizozols, Foresto, Baltic Terra Capital; 274 properties, EUR 5.7 million) undisclosed. (Source: https://www.lfdf.eu/documents)

12. Baltic Terra Capital’s prospectus, November 2025: “The Issuer has not entered into related party transactions.” Not quite false. It’s technically defensible, but practically misleading. All 25 properties were sold to LFDF, another issuer on the same platform. The director simultaneously chairs Dizozols and runs sales at AS JUNO. The same prospectus also omits that 23 of 25 properties came from companies owned by a single individual whose company’s shares had at one point been seized by the State Police on fraud charges (case Nr. 11300012721, hearing scheduled 23 September 2026). (Source: https://company.lursoft.lv/en/baltic-terra-capital/40203653737)

13. Sandbox Funding’s 2024 annual report: no unfavorable or favorable events disclosed after the reporting period. False. Three blanket pledges totaling EUR 30 million were registered 37 days after the balance sheet date, 113 days before the report was signed. (Source: https://company.lursoft.lv/en/sandbox-funding/40203473712)

14. DN Funding Alpha’s 2024 annual report: all related-party disclosure fields blank. False. The company is 100% owned by DN Operator. The report was signed by Ingus Salmiņš, who owns DN Operator via ZIdea. EUR 1.87 million outstanding to investors, not referenced anywhere in the filing. (Source: https://company.lursoft.lv/en/dn-funding-alpha/40203327498)

Three patterns.

Internal contradictions. Entries 1, 2, 3, and 5: the balance sheet reports related-party receivables, the P&L reports related-party interest income, but the disclosure fields deny related parties exist. JUNO’s 2024 filing reports EUR 5.3 million owed by related companies and discloses nothing about related-party transactions.

Shared accountant. Rūta Lacberga prepares the annual reports for AS JUNO (from 2022), LFDF, Baltic Terra Capital, and Foresto. The same person reports the purchase on LFDF’s balance sheet and the sale on the seller’s. Not one of them discloses a material related-party transaction. LFDF’s own management report even carries the header of the wrong company: “AS JUNO 2022.gada pārskats.” Not the only such mistake: Baltic Terra Capital’s first-ever annual report, for a company incorporated in June 2025, contains a note referencing “error corrections, see note No. 25.” There is no Note 25. There is no previous year. The template was carried over from another entity’s report.

Regression. Foresto disclosed a related-company loan in 2023, then deleted the entire section from its 2024 report, the year interest expense tripled. The trajectory is away from compliance.

The Latvian Annual Reports Act requires disclosure of material related-party transactions (Section 52) and off-balance-sheet obligations including pledges (Section 55). Board members are personally responsible for filing accuracy (Commercial Law, Section 174). Under the EU Prospectus Regulation (2017/1129), persons signing the responsibility statement certify that the information “is in accordance with the facts and makes no omission likely to affect its import.”

What happens when it goes wrong

EUR 2.07 million in investor funds are trapped in Ukraine through a borrower called Chain Finance, hit by the war. Rather than recording defaults, the platform moved the obligations into SIA DN Funding Alpha (reg. 40203327498), a wholly-owned subsidiary. The “zero defaults” track record was preserved. Four years later, only EUR 202,500 has been repaid. (Source: https://company.lursoft.lv/en/dn-funding-alpha/40203327498)

At least one investor has had enough. Case C75021625 names both DN Funding Alpha and DN Operator in a civil claim for “damages from investment services contracts.” Hearing: 2 July 2026, Economic Court, Rīga. Open session. This is the first known legal action by an investor against the platform. It did not come from the regulator. (Source: https://www.lursoft.lv/hearings/42103092209?l=en&hearing=1994239)

Debitum’s Trust Score: Zero compliance breaches

Debitum published five blog posts about its three-component issuer scoring system. Five. They explain the methodology, the three-pillar scoring framework, the credit committee, the quarterly reviews. They describe how “transparent, straightforward organizational setups score higher than complex or opaque arrangements.” They describe how they assess “corporate structure” and “transaction structure complexity.” (Source: https://debitum.investments/blog/trust-score-updates-improved-thoroughness-and-transparency/)

Here are the grades. And who owns the companies.

| Issuer | Trust Score | Status |

|---|---|---|

| LFDF | A | Family company |

| Baltic Terra Capital | A | Family company |

| Sandbox Funding | B+ | Debitum owner holds 66.86% |

| Evergreen Capital | B | Independent |

| Triple Dragon | C | Independent |

Here is what an A looks like:

LFDF, with undisclosed intermediaries, undisclosed PEP, and 14 contradicted filings, gets the highest score on the platform.

Baltic Terra Capital, a seven-month-old company with EUR 20,000 in capital, scores A+ on the financial strength component, described as showing “robust initial results.” (Source: https://debitum.investments/blog/7th-block-new-note-issuer-baltic-terra/)

And here is what you need for a B+:

Sandbox Funding gets a cooperation component of A+. Sandbox is registered at Dzirnavu iela 67, Rīga. So is Debitum. Of course they cooperate well. They share an office.

The only issuers scoring below B+ are the two that are actually independent. If I were Triple Dragon, I would be throwing an absolute fit.

On 13 August 2025, after everything documented in this article was already in the public record, the quarterly review found “zero compliance breaches across all active partners.” (Source: https://debitum.investments/blog/quarterly-partners-trust-score-update-stability-prevails/)

LFDF’s “advanced sourcing and valuation methods ensure that only high-potential properties are acquired.” The prospectus does not describe how those methods produced a 50% markup to family companies.

“Every euro invested is backed by tangible, income-generating forest properties.” The prospectus explicitly excludes forest properties from the pledge. (Source: https://www.lfdf.eu/documents)

Where is the regulator?

Debitum holds MiFID II authorization from Latvijas Banka, Latvia’s central bank and financial regulator. Both the LFDF and Baltic Terra Capital prospectuses were approved by Latvijas Banka. So far, there has been no public regulatory action. The first legal challenge came from an investor.

Either the regulator approved this, missed it, or couldn’t stop it.

Maybe this is all fine. Maybe there’s a perfectly reasonable explanation for why a former MP’s family collects a 50% markup on every piece of forest bought with investor money. Maybe the regulator approved two prospectuses that omit five related intermediaries because those intermediaries aren’t relevant. Maybe fourteen false filings across eleven companies, all prepared by the same accountant, are just a coincidence. Maybe a finance ministry official can beneficially own a EUR 37.9 million investment fund and nobody needs to know about it.

Or maybe it’s time the regulator starts looking into this.

Disclosure

The author received an unsolicited anonymous communication in January 2026 flagging some of the same issues. All findings in this article were independently verified from public records. Time-stamped archived copies of all cited sources exist.

About the Author

Karsten is a Latte-and-Volvo kind of stay-at-home dad to two young kids. He spends naptime watching Bluey, bedtime reading annual reports of Latvian crowdfunding companies, and the rest reassuring his wife that EUR 2,234.69 in Latvian corporate registry lookup fees is a perfectly reasonable household expense.

Like other geriatric Millennials, he can be reached by e-mail, on the BeyondP2P Telegram group, or in the parents WhatsApp group for his kiddos (Go Busy Bees!).